Explained: What is GST e-invoicing? What’s changed from April 1, 2025? Premium

The Hindu

GST Council approved e-invoicing system for B2B invoices, with new rules and regulations, mandatory for all taxpayers from April 1.

The Story so far: The GST Council of India approved and rolled out the ‘e-invoicing’ or ‘electronic invoicing’ eco-system in a phased manner for reporting of business-to-business (B2B) invoices to GST portal. As there were no existing standards/formats then, a standardised format was introduced across the country, after having several consultations with trade/industry bodies as well as Institute of Chartered Accountants of India. Since then, several changes were also being made to the GST e-invoicing rules and regulations. Before getting into the details of what is GST e-invoicing and how this works, let’s first check out the new rules.

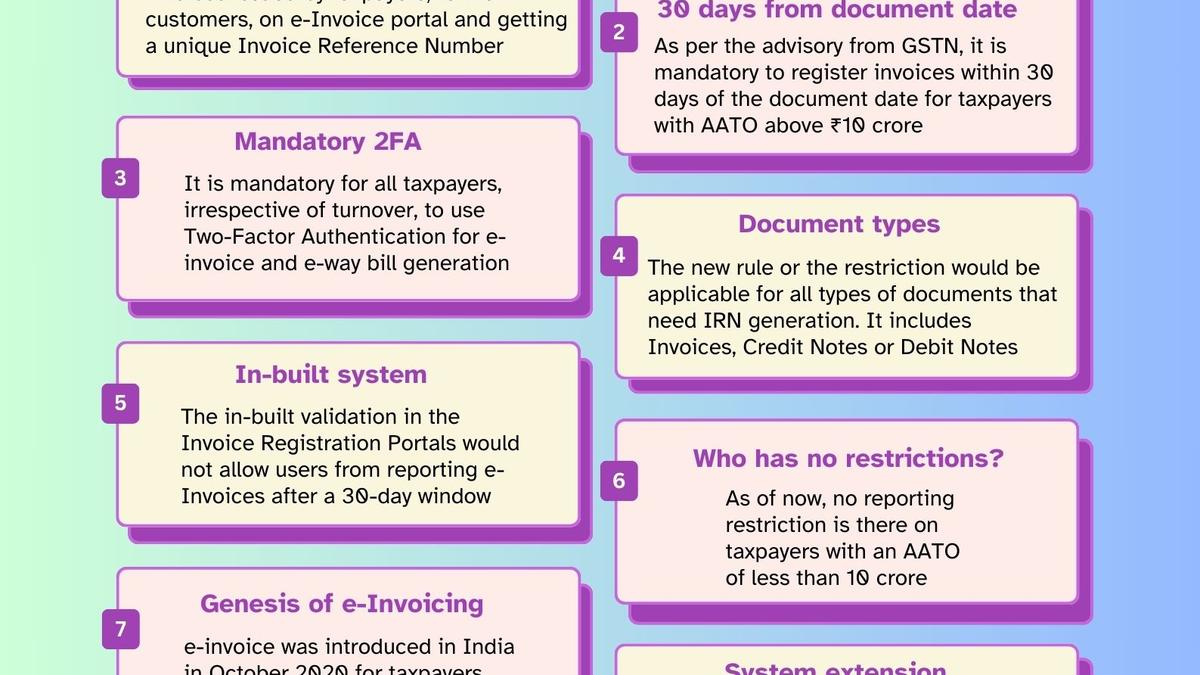

From April 1, 2025, business houses with an Annual Aggregate Turn Over (AATO) of ₹10 crore and above must report/upload e-invoices to the Invoice Registration Portal (IRP) within 30 days from the date of issue of the document. Earlier, this rule was meant only for business houses with an AATO of more than ₹100 crore. As the turnover threshold has been reduced drastically, large number of business houses must comply with this 30-day deadline.

Currently, there are no strict regulations on the deadline of reporting invoices. Therefore, a few businesses upload invoices in a delayed manner, thereby creating discrepancies in Input Tax Credit (ITC) claims and overall tax compliance. But now, the in-built validation in the IRPs would not allow users from reporting e-Invoices after the 30-day window. Late submissions would automatically be rejected, with consequences leading to potential penalties and financial setbacks.

From April 1, it is mandatory for all taxpayers, irrespective of turnover, to use Two-Factor Authentication (2FA) system for e-invoice and e-way bill generation.

GST e-invoicing involves reporting of B2B invoices and export invoices issued by taxpayers, to their customers, on the Union Government’s e-invoice portal and getting a unique Invoice Reference Number (IRN). This doesn’t mean that the invoice would be generated by the government portal itself. Further, e-invoice doesn’t simply mean that the invoice would be in a soft copy version such as PDF. According to the GST portal, “It’s a faceless system with major thrust on API integration so that the eco-system can exchange the data electronically.”

The standard of GST e-invoice was first approved by the GST Council in its 37th meeting held on September 20, 2019. e-Invoicing was introduced in India, in a phased manner, in October 2020 for taxpayers with Annual Aggregate Turn Over (AATO) of more than ₹500 crore. Later, in January 2021, the eco-system was extended to taxpayers with AATO between ₹100 and ₹500 crore.

The types of documents that need to be uploaded for IRN generation include GST Invoices, Credit Notes or Debit Notes related to B2B supplies and exports.

OpenAI has signed a new deal to sell access to its AI models to U.S. defence and government agencies through Amazon’s cloud unit for classified and unclassified work, the ChatGPT maker said

Samsung Electronics said on Wednesday that it expects to start volume production of Tesla’s chips

The Trump administration said in a Tuesday court filing that the Pentagon’s blacklisting of Anthropic was justified and lawful

Mastercard Move aims to simplify cross-border payments for SMEs and students in India, enhancing efficiency and reducing costs.

SBI raises ₹6,051 crore through 10-year bonds, attracting strong investor demand with a 7.05% coupon rate.

In February, as per government data, domestic LPG production was slightly more than 1 million tonne.

Union Government urges States and UTs to expedite approval of gas pipeline projects to promote piped natural gas usage.

Parliamentary panel criticizes Ministry of Planning and Niti Aayog for persistent underutilization and poor financial management practices.

LPG consumption in India dropped 17.7% in March due to war-related supply disruptions, impacting household cooking gas availability.

LPG eKYC is required only for unauthenticated customers, clarifies the Ministry of Petroleum and Natural Gas.

India's second LPG carrier, 'Nanda Devi', arrives at Gujarat's Vadinar port, carrying 46,500 metric tonnes of gas.

European publishers, tech firms and startups have urged EU antitrust regulators to wrap up a near two-year probe into Alphabet unit Google’s alleged favouring of its own services in online searches and impose a fine on the tech giant.

OpenAI is in advanced talks with private equity firms including TPG, Advent International, Bain Capital and Brookfield Asset Management to form a joint venture