Putting Budget 2023 into perspective

The Hindu

The Union Budget assumes a nominal GDP growth of 10.5% in 2023-24, which implies a projected inflation rate of just 4%, given the economic survey’s baseline real GDP growth projection of 6.5%. How does this fare against the figures of the previous governments?

As per the latest economic survey, the Indian economy is set to attain a real GDP growth of 7% in 2022-23, with both the retail and wholesale inflation rates falling below 6% in the months ahead. The Union Budget presented in this backdrop assumes a nominal GDP growth of 10.5% in 2023-24, which implies a projected inflation rate of just 4%, given the economic survey’s baseline real GDP growth projection of 6.5%. This reflects official optimism regarding the Indian economy remaining in a macroeconomic sweet-spot of declining inflation and high growth, even as the rest of the world experiences a growth slowdown alongside sticky inflation.

The economic survey has predicted a fresh cycle of investment-led growth led by the private corporate sector, supported by increasing credit from the banks, coming out of the bad loans overhang following the apparent clean-up of their balance sheets. Rather than relying upon such rosy predictions, however, the Finance Minister has announced a sharp increase in capital expenditure in the Union Budget, seeking to “crowd-in” private investment especially in infrastructure sectors like railways, roads and power plants. On the other hand, subsidies on food, fertiliser, petroleum and interest subsidies, along with outlays on welfare schemes like the MGNREGA have been reduced quite significantly, indicating higher prices of cereals, LPG cylinders and fertilisers like urea in the days to come. The overall impact of such expenditure switching may turn out to be inflationary.

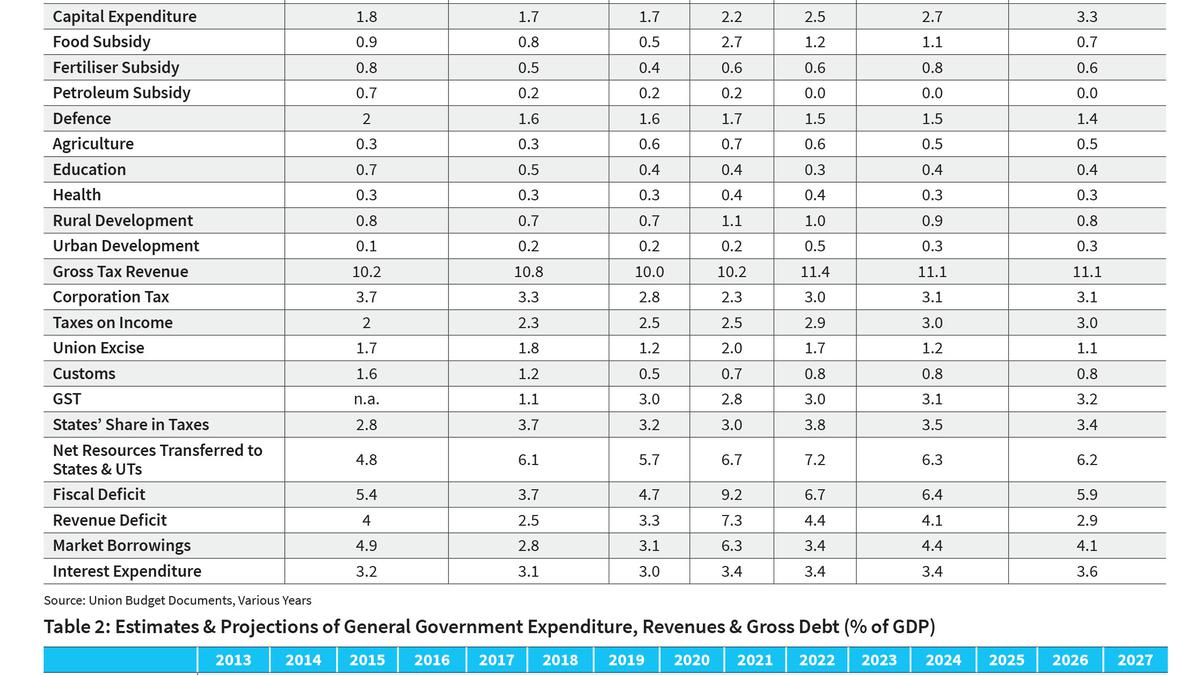

A longer-term assessment of the Union Budgets is presented in Table 1, which enables us to compare the present government’s fiscal strategy in the post-pandemic period with the fiscal record of the UPA-II and NDA-I governments. As can be seen from Table 1, while the total central government expenditure (annual average) fell from 15% of the GDP during the UPA-II era to below 13% during the NDA-I government’s tenure, the recession precipitated by the COVID-19 pandemic forced a substantial increase in total expenditure to 17.7% and 16% of the GDP, in 2020-21 and 2021-22, respectively. Total expenditure has reduced moderately since then, to around 15% of GDP.

While capital expenditure has been enhanced significantly since 2020-21, beyond the levels attained by the UPA-II and NDA-I regimes, subsidies on food, fertiliser and petroleum have been reduced from 2021-22. Defence expenditure, which was 2% of the GDP on average under the UPA-II government Budgets and 1.6% of GDP under the NDA-I, has fallen to 1.5% of GDP in 2022-23. As a proportion of the GDP, while expenditure on agriculture seems to have increased during the NDA-II government’s tenure, mainly on account of the PM-Kisan cash transfer scheme, expenditure on education has reduced quite significantly compared to the UPA-II era. Expenditure on rural development and health seems to have remained at the same level. The increase in capital expenditure is mainly focussed in transport and energy sectors.

The reason why the government has to cut subsidies and welfare expenditures to increase capex on infrastructure is because of inadequate revenues, which have remained to be the principal constraint on public expenditure. Table 1 shows that gross tax revenues as a share of GDP barely rose from 10.2% under the UPA-II period to 10.8% under NDA-I and then fell to around 10% during the first two years of the NDA-II government. It is only in the post-pandemic period, since 2021-22, that gross tax revenues have crossed 11% of GDP.

It can be noted further that the corporate tax collection as a share of GDP fell from 3.7% of the GDP under the UPA-II to 3.3% of the GDP under the NDA-I, and came down further to 2.3% of the GDP in 2020-21 following the sharp corporate tax cuts introduced in 2019. The post-pandemic recovery has led to enhanced tax collections, but corporate tax collections remained at 3.1% of the GDP in 2022-23.

While corporate taxes in the GDP have declined under the NDA rule, the share of income taxes in the GDP has risen progressively to reach 3% of the GDP in 2022-23. Revenues from personal income taxes becoming almost equal to corporate tax revenues point towards a regressive taxation regime, which perhaps compelled the Finance Minister to provide a few concessions to income tax payers in this year’s Budget. However, going by the Finance Minister’s speech, revenue foregone due to those concessions is projected at only ₹35,000 crore, in the backdrop of income tax collections of ₹8,15,000 crore (RE) in 2022-23. Moreover, the dual income tax regime with a multiplicity of slabs has unnecessarily complicated the income tax structure.

Vodafone Idea's board approves FPO offer price at Rs 11 per share, raising Rs 18,000 crore for debt-laden telecom operator

India seeks details from Singapore and Hong Kong on spice ban, focusing on quality concerns and corrective actions.

The local unit opened at 83.37 against the greenback. The unit hit an intra-day high of 83.28 and a low of 83.39 against the greenback

Equity benchmark indices Sensex and Nifty closed higher for the third session in a row, following gains in telecom, tech and consumer durable shares amid a firm trend in the global markets.

SEBI finds offshore funds violating disclosure rules and investment limits in Adani Group, some opt for penalty settlement.

Ensure children up to 12 years are allocated seats with their parents in flight: DGCA tells airlines

DGCA mandates airlines to seat children under 12 with parents, revises air transport circular for unbundled services

Lok Sabha elelction: Congress criticizes PM Modi for wealth distribution, Jairam Ramehs says inclusive economic growth is possible only under an INDIA bloc government.

Lok Sabha elelction: Congress criticizes PM Modi for wealth distribution, Jairam Ramehs says inclusive economic growth is possible only under an INDIA bloc government.

New Delhi stock market continues winning streak, Sensex up 411.27 points, Nifty advances 111.15 points, global markets firm.

Rupee strengthens against U.S. dollar in early trade as market sentiment improves, supported by domestic equities.

FSSAI samples spices from all brands, including MDH and Everest, amid quality concerns flagged by Singapore and Hong Kong.